What Mortgage Rate Will Get More Buyers Moving?

About 5.5 million more households would be able to afford a home if rates drop to this magic number.

MARKET CONDITIONSHOUSING FORECASTMORTGAGE RATES

What Mortgage Rate Will Get More Buyers Moving?

REALTOR® Magazine, article by Melissa Dittmann Tracey | July 17, 2025

About 5.5 million more households would be able to afford a home if rates drop to this magic number. NAR’s latest housing forecast shows when the market may get there and where you can find opportunities for business growth.

Home buyers wishing for lower mortgage interest rates may eventually get their wish, but for now, they’ll have to decide whether it’s better to wait or jump into the market.

Buyers remain highly sensitive to interest rates. Many blame today’s rates for a subpar selling season, and economists say that when rates begin to fall, a wave of pent-up demand could be unleashed, potentially driving a surge in home sales.

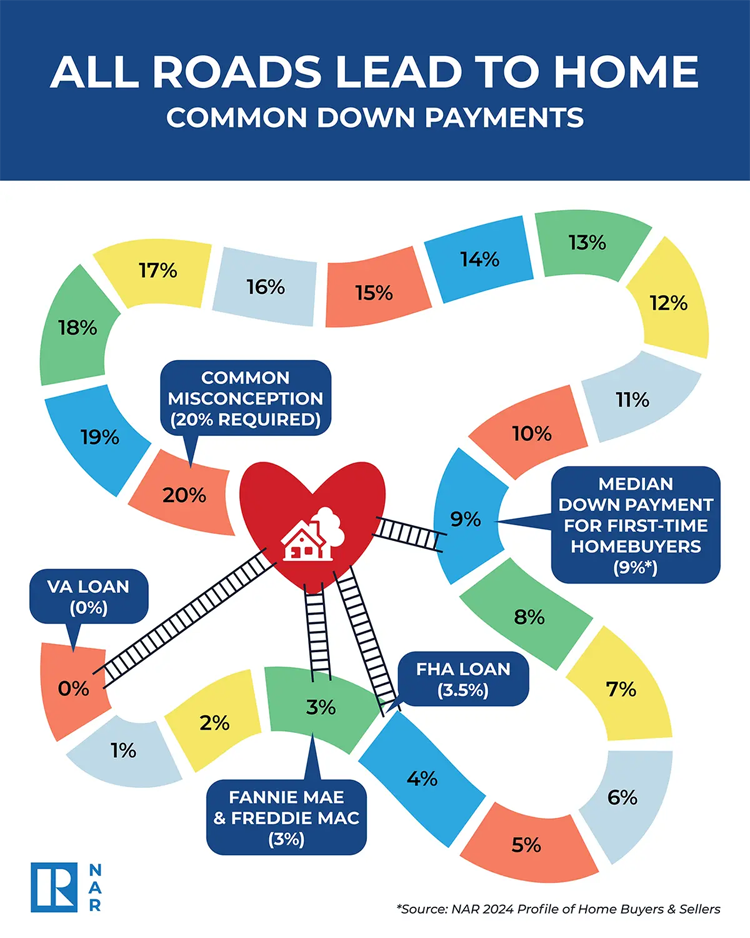

National Association of REALTORS® economists say a 30-year fixed rate mortgage of 6% would make the median-priced home affordable for about 5.5 million more households—including 1.6 million renters. If rates were to hit that magic number, it’s likely that about 10%—or 550,000—of those additional households would buy a home over the next 12 or 18 months, according to new data from NAR.

Summit Draws Thousands

At a July 16 Real Estate Forecast Summit, NAR’s economists shared their forecast and demonstrated a new member exclusive—an interactive Metro Market Statistics Dashboard that tracks housing and economic data in more than 200 metro areas. The dashboard indicates that Atlanta, Dallas, Minneapolis, Cleveland and Kansas City, Mo.-Kan., would be among the markets seeing the largest uptick in home sales if rates were to drop to 6%.

Thousands of members joined the summit webinar, no doubt hoping for good news on rates, sales, and the general economy. And there are positive economic indicators, NAR Chief Economist Lawrence Yun told summit attendees.

Seven million more jobs have been added to the U.S. economy since COVID, and wages have risen. “[Although] many people are waiting for mortgage rates to go down to make it more affordable to get into the market,” Yun said, “buyer demand can quickly change depending on how the mortgage rate changes.”

The 30-year fixed-rate mortgage has remained stubbornly high this year, averaging 6.72% as of July 10, according to Freddie Mac. But the Federal Reserve is expected to cut its benchmark short-term rate four to six times over the next 12–18 months, which could prompt mortgage rates to fall.

NAR forecasters say rates could dip to that projected homebuying sweet spot of 6% by 2026. That would drive home sales up 14% in 2026, they say.

So, Should Buyers Wait?

Buyers who are holding out for lower mortgage rates may be missing a key opening in the market.

Following years of declines, housing inventories are finally rising across the country, giving once inventory-starved metros more options for prospective buyers. Nationally, inventory of existing homes was up 20% in May compared to a year earlier—but some markets saw even sharper increases, with inventory levels up as much as 80% annually, Yun said.

As a result, home shoppers may find they have more bargaining power than in recent years.

While home prices are still rising, the pace has slowed significantly compared to recent years. Some real estate professionals are even reporting more price drops, as seller competition heats up. NAR predicts that, on a national basis, home prices will rise modestly—by about 1% in 2025—before accelerating to a projected 4% increase in 2026.

Yun noted that current homeowners remain the biggest beneficiaries of the housing market, enjoying record-high real estate net worth. “Through real estate, more Americans are gaining financial security,” Yun said. “Real estate net worth is on solid ground, based on the low delinquency rate and even lower foreclosure rate conditions.”

Using NAR’s new dashboard, members can see just how owners in their market have benefited. In Phoenix, for example, homeowners gained an average of $320,860 in equity over 10 years of ownership—wealth that non-homeowners are missing out on.

The Housing Forecast: 2025 and 2026

Because mortgage rates remain stagnant, NAR downgraded its housing forecast for the remainder of 2025—but upgraded its forecast for 2026 on the expectation that rates will begin to come down. Yun presented the following outlook for the housing market:

Existing-home sales:

2025: +3%

2026: +14%

New home sales:

2025: +5%

2026: +5%

Median home prices:

2025: +1%

2026: +4%

Mortgage rates:

2025: 6.7%

2026: 6%

Jobs:

2025: +1.6 million

2026: +2 million

Identifying Real Estate Growth Opportunities

Although home sales were sluggish iqan the first half of the year, economists are noting signs of momentum in several key areas of the market. Here's where to watch for growth:

Migration trends south—and elsewhere: The U.S. population grew by nearly 1% in 2024—the fastest rate since 2001, said Anat Nusinovich, an NAR economist, during the summit. The largest population gains occurred in:

Washington, D.C.

Florida

Texas

Utah

South Carolina

Nevada

Idaho

North Carolina

Delaware

Arizona

The South alone added nearly 1.8 million people in 2024, making it the fastest-growing region in the U.S. However, other regions, particularly the Midwest, also are showing signs of strength, Nusinovich said, noting job growth and increasing demand for home purchase loans in metro areas like Des Moines, Iowa; Indianapolis; and Omaha, Neb. “With additional rate cuts expected from the Fed this year, we expect to see continued growth not just in the South but across more areas of the country,” she said.

First-time buyers return: First-time buyers made up only 24% of the market last year—a record low, compared to the historical norm of about 40%. However, they’re slowly returning, currently accounting for 30% of home purchases in May, according to Jessica Lautz, NAR’s deputy chief economist. She attributed the rebound to more stable mortgage rates (hovering in the mid-to-high 6% range since January) and increased housing inventory. “Having a more predictable interest rate may have given first-time buyers the confidence to enter the market,” Lautz said.

She encouraged real estate professionals to:

Educate buyers on low down payment options (e.g., assistance options listed at Down Payment Resource or Federal Housing Administration loans).

Dispel the myth that a 20% down payment is required—most first-time buyers put down only 9%.

Highlight how increased inventory could open more homebuying opportunities for them.

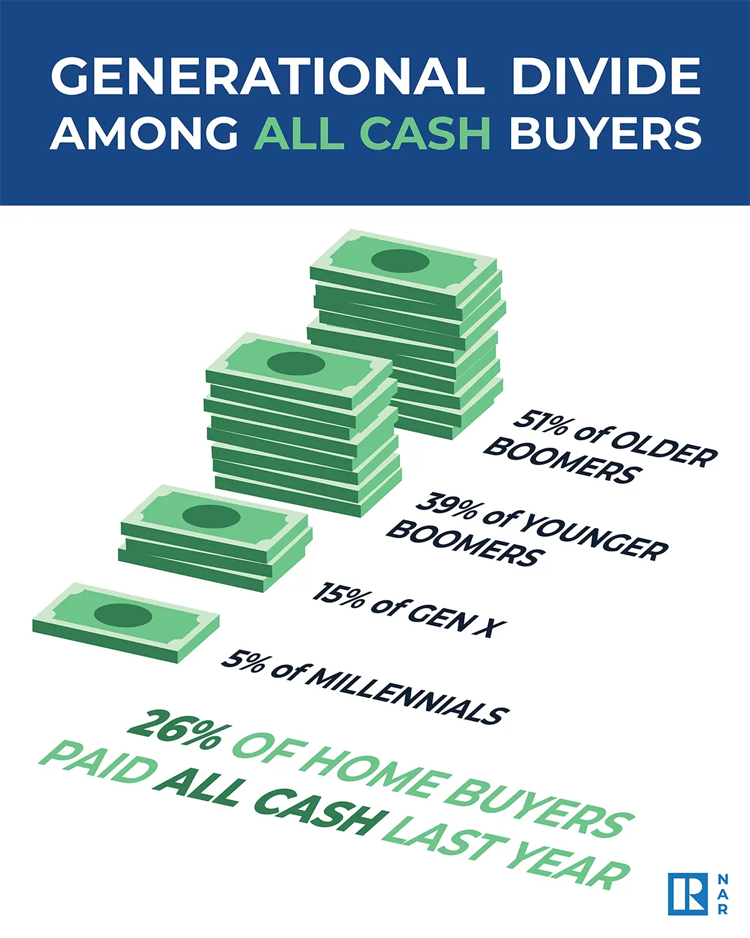

All-cash buyers stay strong: All-cash purchases now make up over 25% of the housing market, with one-third of repeat buyers—primarily baby boomers—buying homes without a mortgage. Many are using equity from prior home sales, Lautz noted.

She advised agents to connect with potential all-cash buyers by helping homeowners assess their home equity with the help of NAR’s Metro Market Statistics Dashboard. Also, recognize that the top reason people are moving lately isn’t for jobs, but to be closer to family—a trend led by boomers, she said.

Interestingly, Lautz noted that one in 10 first-time buyers also are paying all-cash for a home purchase, drawing from personal savings, inheritance, financial gifts from their parents and investments, like stocks or 401(k)s.

Copyright © 2026 Kenneth Sells Nashville | Nashville Kenneth All Rights Reserved. All information deemed to be accurate but not guaranteed; Buyer's/Seller's Agent to verify all pertinent information.

KENNETH M BARGERS LIC 318311 (615) 512-9836 M kb@kennethsellsnashville.com E realestate@nashvillekenneth.com E kennethsellsnashville.com W nashvillekenneth.com W

ADARO Realty LIC 261466 (615) 376-1688 O 1187 Old Hickory Blvd, Suite 125, Brentwood TN 37027 A adarorealty.com W an agency of Crye-Leike Real Estate Services